It’s time to start preparing your annual HMDA submission. CrossCheck partners with lenders to make the process seamless, offering systemic and manual file reviews, ongoing monitoring, fair lending disparity analysis, and tailored training. Contact our team for more information.

The regulatory pendulum often swings, and with current attention from federal regulators partially diverted, some lenders may feel tempted to deprioritize compliance efforts. However, maintaining a robust compliance program is not just about staying on the regulators’ good side; it safeguards your institution from potential violations, enhances operational efficiency, and reinforces fair lending practices. Whether federal agency scrutiny is heightened or relaxed, a commitment to compliant lending is non-negotiable, and that commitment should include the Home Mortgage Disclosure Act (HMDA)/Regulation C.

A proactive approach to HMDA enables institutions to stay ahead of regulatory expectations. A strong HMDA compliance program includes 1) board and management oversight, 2) policies and procedures, 3) training, and 4) monitoring and reporting. These four pillars form the foundation of a robust program that ensures institutions accurately collect, report, and disclose HMDA data, fulfilling the Act’s purpose of transparency and addressing community housing needs.

The third pillar, training, is crucial for ensuring that all relevant personnel understand their responsibilities under HMDA. Training should be tailored to distinct roles and responsibilities and should be updated regularly to reflect changes in regulations or business practices. Effective training should include examples, or scenarios, to explain how lenders should accurately report specific fields on their Loan/Application Register (LAR), including when to report a field as not applicable (“NA”).

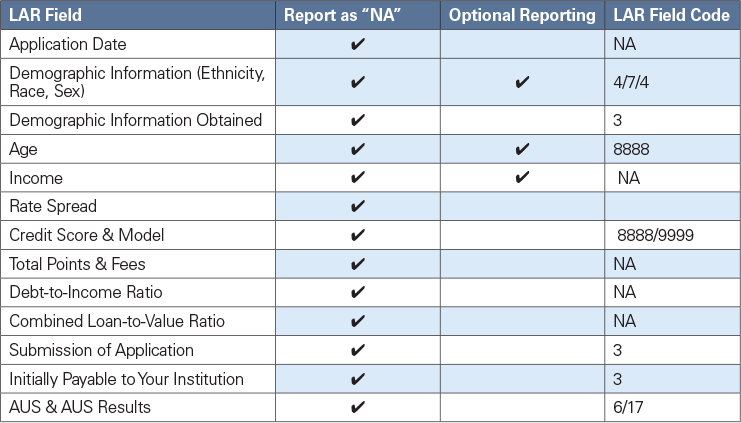

The challenges of reporting “NA”

The HMDA reporting requirements are detailed and nuanced, with specific instructions for each data field. One challenging aspect of HMDA compliance is navigating the complexities around accurately reporting “NA” for specific fields on the LAR. Lenders must carefully interpret these rules to determine when “NA” is appropriate, which can be difficult without deep familiarity with the regulation.

A particular loan type, purpose, and status (e.g., application, origination, denial, withdrawal) requires different consideration. For example, some LAR fields may not apply to certain loan products such as open-end lines of credit or reverse mortgages, and determining these distinctions can be confusing. Further, despite detailed instructions, some LAR requirements leave room for interpretation. For instance, determining whether a field is truly “NA” or should be left blank can be unclear, leading to potential errors on your LAR.

Many lenders rely on automated systems to populate their LAR. Errors can occur if these systems are not properly configured to account for “NA” scenarios. Manual overrides in loan origination systems may be needed, which increases the risk of inconsistency. Some data points required under HMDA/Regulation C also overlap with other regulatory requirements (e.g., Truth in Lending Act/Regulation Z or Equal Credit Opportunity Act/Regulation B), which can create confusion about when “NA” is appropriate under HMDA versus other rules.

Reporting “NA” versus other field values

Understanding when “NA” is the appropriate entry is vital to achieving accuracy and maintaining consistent reporting of your LAR. Following are six areas where lenders have the opportunity, but may be uncertain as to when, to report “NA” or a different field value on their LARs.

Purchased loans — NA reporting

1. Property address

If the address of the property securing the loan is unknown or undetermined at closing (e.g., a construction loan for which an address is not assigned to the lot/location as of closing, or a manufactured home without an identified site as of closing), or the property address has not been provided before the application is denied, withdrawn, or closed for incompleteness, Regulation C provides that “NA” should be entered for Property Address.

HMDA reporting is never quite that simple and straightforward, though, and reporting Property Address can be particularly complicated because it includes multiple fields and overlaps with the Property Location data point.

There are four Property Address fields: Street Address, City, State, and Zip Code. Reporting the State field is subject to the requirements both for Property Address under § 1003.4(a) (9)(i) and Property Location under § 1003.4(a) (9)(ii). Even where “NA” should be reported for Property Address (because, for example, the Street Address is unknown), the State field for Property Address should only be reported “NA” if State is also being reported as “NA” for Property Location — there is only one field for reporting State on the LAR.

Consider the following three examples:

- TBD, Atlanta, GA 30305

- Main Street, Culpepper, VA 22701

- Lot #5, Wichita Falls, TX 76302

The specific Street Address is not known; therefore, “NA” should be reported for all of the Property Address fields except State, assuming State is required to be reported for Property Location.

In addition, Property Address, but not Property Location, is a data point covered by the partial exemptions under the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA). This means that an institution eligible for a partial exemption could choose to report “Exempt” for only the Street Address, City, and Zip Code fields, as the State field is not covered under the partial exemptions. Even if an institution qualifies for partial exemptions, it may still choose to report the partially exempt Property Address fields (Street Address, City, and Zip Code) voluntarily.

2. Income

Determining when reporting “NA” is acceptable for the Income field can cause uncertainty and confusion for HMDA reporters, as there are multiple scenarios in which this may apply. You should report Income as “NA” when the:

- Income was not considered, or would not have been considered, in making the credit decision (e.g., asset-based lending product, reverse mortgages)

- Applicant or co-applicant is not a natural person (e.g., LLC, corporation, etc.)

- Loan is secured or proposed to be secured by a multi-family dwelling (5 or more units)

- Bank chooses not to report Income for loans it purchased

- Applicant or co-applicant is an employee of the bank, even if the applicant income was used in making the credit decision

The first two bullets above are often areas where lenders can misstep and report “NA” when an income value should be reported. Reporting “NA” for Income is only acceptable if borrower income, in any amount or form, was not considered at all in the credit decision. HMDA guidelines are clear that credit underwriting details such as income, as well as credit score, debt-to-income ratio, and combined loan-to-value ratio need to be reported if they influenced the credit decision in any way, even if they were not the dispositive, or a deciding factor in underwriting the loan. For example, in situations where the primary borrower is an entity and the co-borrower is a natural person, and the co-borrower’s income was used in the credit decision, you should report the co-borrower’s income.

3. Rate spread

Rate Spread is another LAR field that is a common source of confusion and more susceptible to error because it is a calculated field that relies on other, non-reportable, data being accurate. However, determining when to calculate and report Rate Spread or report that the field is “NA” for a loan or application, can also be challenging. Lenders can report the Rate Spread as “NA” in the following scenarios:

- Loan types: If a loan is an assumption, reverse mortgage, or a purchased loan, the Rate Spread is reported as “NA.”

- Loans not subject to regulation Z: If a loan is not subject to Regulation Z, the Rate Spread is reported as “NA.” Such loans include business-purpose loans, agricultural-purpose loans, and loans to non-natural persons.

- Applications that did not result in origination: If the application was denied, withdrawn, or closed for incompleteness, except for cases where the application was approved but not accepted, the Rate Spread is reported as “NA.”

These rules ensure that lenders only report Rate Spread data when it is relevant and required.