It is hard to believe that the TILA-RESPA Integrated Disclosure (TRID) rules, also known as Know Before You Owe (KBYO), have been in effect since October 2015, almost seven years ago. Although the industry has digested the requirements and configured loan systems to assist with compliance—human error, unexpected events, and miscommunications all contribute to errors that can increase the potential for fee tolerance violations. Personnel may think the bank’s loan systems will automatically produce compliant disclosures, and while good system controls certainly help, errors still occur. Whether your institution is large or small, you’ll want to be sure not to make any of these eight common errors.

- Failing to fully document change in circumstance.

- Including undetected reimbursable fee tolerance violations on Loan Estimates and Closing Disclosures.

- Stating lender credits on loan disclosures improperly.

- Failing to provide Loan Estimates when applications do not result in an originated loan.

- Using standard and alternative format disclosures for the same transaction.

- Failing to obtain and document the borrower’s intent to proceed.

- Failing to retain adequate evidence of timely delivery of Closing Disclosures.

- Including an expiration date of estimated closing costs on revised Loan Estimates.

1. Failing to fully document change in circumstance

A valid change in circumstance is defined in Regulation Z as an extraordinary event beyond the control of any interested party, reliance by the creditor on information that has become inaccurate, or new information becoming available to the creditor. Failing to obtain basic information on the transaction would not meet this definition so it is critical to obtain accurate information on the borrower, subject property, and purpose of the loan at the time of application.

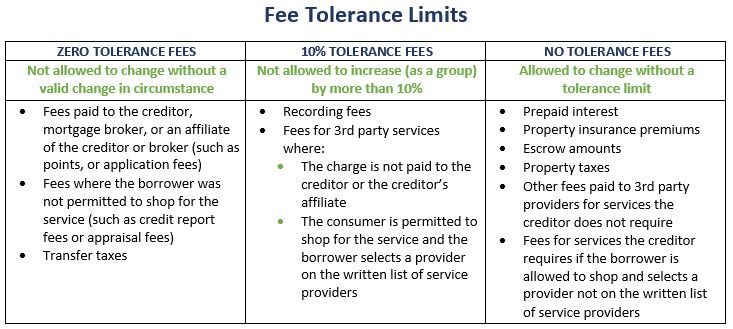

If a valid change in circumstance does occur, fees directly related to the change are allowed to increase (within reason). However, without a valid change in circumstance, fees are only allowed to change within certain limits, as described in the table on the next page.

A common error is failing to retain adequate documentation to support that a change in circumstance has occurred. Regulation Z requires this documentation to include the original estimate of the cost, the reason for the revision, and how the change affected settlement costs. Although not required, maintaining a standard change in circumstance form outlining the details of the change will help document compliance with TRID rules. Including a check box for the most common causes for change in circumstance can help clearly identify the cause of the change, such as locking the interest rate, a borrower requested change, or a change in loan amount, for example. Including an “other” option will require close monitoring so it is not misused as a catch-all or used when a change in circumstance is not valid.

Another challenge is to ensure that only fees directly related to the change in circumstance are increased when providing a revised Loan Estimate. Increasing other fees on the revised disclosure that are not directly related to the change of circumstance could result in tolerance issues that will require a cure. For example, an increase in the loan amount is typically not directly related to the appraisal fee, so the tolerance limit for the appraisal fee in this situation cannot be reset. If errors are made that exceed allowed thresholds, they are required to be reimbursed to borrowers.

2. Including undetected reimbursable fee tolerance violations on Loan Estimates and Closing Disclosures

Increases to loan fees after the original Loan Estimate is provided or when Closing Disclosures are issued are subject to limitations, and fees may only increase within the applicable tolerance limits discussed above. Increases in fees can be caused by human error such as fees that are:

- Unintentionally omitted from initial or revised loan disclosures;

- Disclosed as a fee the borrower shopped for when in fact the borrower did not shop for that particular service; or

- Under-disclosed as a result of insufficient information that is obtained regarding the loan during the application process.

Strong internal controls should be established to ensure all applicable fees are included on the initial Loan Estimate and disclosed in the appropriate section of the disclosure. All standard loan fees required by your institution such as origination charges, credit report fee, appraisal fee, tax service fee, flood-related fees, and applicable title-related fees should be included on all disclosures. If fees are omitted from the initial Loan Estimate, especially zero tolerance fees, then funds may need to be reimbursed to borrowers.

Errors also occur if fees are changed when a revised loan disclosure is issued, but the increase in the fee was not permitted by the TRID regulations. Revised Loan Estimates are only required after the interest rate is locked or when the institution is resetting the tolerance limits after a valid change in circumstance has occurred. Providing revised disclosures for informational purposes to correct minor or technical items can increase the potential for omitting a fee or making a mistake with the amount of a fee. Management should ensure revised disclosures are delivered to borrowers as required by the regulation, but when not required, institutions should ensure that the benefit of providing an updated informational disclosure outweighs the potential for making an error that could result in reimbursements to the customer. Providing frequent informational disclosures when not required increases the potential of an error occurring that requires reimbursement to the borrower. Establishing effective system controls can help ensure fees are disclosed in the correct section of the Loan Estimate, thereby avoiding technical violations.

Fee tolerance violations also occur when the borrower is allowed to shop for services, such as title fees, and then these fees are listed in the wrong section of the disclosure. Fees are reported in separate sections of the disclosures as those the borrower shopped for, and those the borrower did not shop for. If the service provider used was one that the institution included on the written list of settlement service providers given to the applicant, then the applicant did not shop for this service and it should be disclosed in Section B of the Loan Estimate and Closing Disclosure. However, if the service provider used was not on the list, then the fee was shopped for and should be included in Section C of these disclosures. Listing a fee in the incorrect section can cause a fee tolerance violation. Fees in Section B (Services You Cannot Shop For) are subject to zero tolerance limitations and fees in Section C (Services You Can Shop For) are subject to 10% tolerance limits. Incorrectly listing a fee the customer did not shop for in Section C for an amount greater than the amount initially disclosed increases the likelihood of having to reimburse funds to the borrower.

3. Improperly stating lender credits on disclosures

Failing to treat lender credits correctly on loan disclosures is another common issue. TRID rules permit lender credits to decrease only if there is an accompanying change in circumstance or another triggering event. Errors occur when a specific lender credit is listed on loan disclosures to cover certain fees, such as the appraisal, and then the cost for these fees decrease on revised loan disclosures. TRID does not allow the lender credit to decrease in this situation as it has the same effect as increasing a fee. Lowering the lender credit when not permitted leads to a borrower reimbursement. The CFPB published ten frequently asked questions on how to disclose lender credits on loan disclosures and this guidance can be helpful to personnel responsible for producing loan disclosures (https://www.consumerfinance.gov/compliance/compliance-resources/mortgage-resources/tila-respa-integrated-disclosures/tila-respa-integrated-disclosure-faqs/).

4. Failing to provide Loan Estimates when applications do not result in an originated loan

TRID rules require that the Loan Estimate and other early disclosures be delivered to applicants no later than the third business day following the day the application is received. A common error is not providing the required Loan Estimate within three business days of application in situations where the loan does not close. TRID rules define an application as when six pieces of information are received by the creditor: borrower name, income, social security number, property address, estimated property value, and loan amount. Loan origination systems should have rules embedded to track the application date. If an application is denied or withdrawn within three business days of receiving the application, then the Loan Estimate disclosure is not required to be provided. However, errors occur when the loan is not actually denied or withdrawn until after three business days from receipt of the application and personnel fail to provide early disclosures within the required time frame.

A process should be in place to document when a loan application is denied or withdrawn within three days of receipt, and therefore initial disclosures were not required to be provided.

5. Using standard and alternative format disclosures for the same transaction

Loan systems are often programmed to adjust the format of the disclosures based on system parameters and the data entered into the system. The standard format includes:

- Information that is applicable to a purchase transaction as it will list detailed information on the amount of cash required for closing;

- Any needed adjustments between the buyer and seller (such as for prorated real estate taxes); and

- Information about the seller.

The alternative format is used for transactions without a seller and will include information on whether the borrower will be receiving cash at closing or if the borrower is required to bring cash to closing. It will also include details on the disbursements of the loan proceeds.

TRID rules allow for use of the standard disclosure format for both loan purchase transactions and refinance transactions. However, TRID states that if the alternative format of the Loan Estimate is used for a transaction without a seller, then the Closing Disclosure must also use the alternative format. In other words, an institution is not allowed to use the alternative format for the Loan Estimate and the standard format for the Closing Disclosure. This error is usually caused by entering the incorrect loan purpose into the system. An example is when the loan purpose is entered as a refinance when in reality there is a seller involved in the transaction. This could cause the system to generate the Loan Estimate in the alternative format and then when the system is corrected to a purchase transaction, the Closing Disclosure is produced using the standard format. Unfortunately, delivering a Loan Estimate using the incorrect format cannot be easily resolved so it is important to issue Loan Estimates with the proper format.

6. Failing to obtain and document the borrower’s intent to proceed

Institutions are required to document the fact that the borrower communicated an intent to proceed to satisfy the record retention requirements within Regulation Z. There are no specific requirements on how this intent is documented, so it can be memorialized in an email, on a checklist, a field in the loan origination system, or a written notice from the borrower. Errors have occurred when personnel fail to follow established procedures and do not retain evidence. TRID rules also require the intent to proceed be communicated prior to collecting any loan fees other than the credit report fee. Controls should be in place to prevent collecting any fees from the borrower until the borrower has communicated the intent to proceed, and it has been evidenced in the loan file or loan origination system.

7. Failing to retain adequate evidence of timely delivery of Closing Disclosures

TRID rules require that borrowers receive a Closing Disclosure at least three business days prior to the loan closing. It is important that evidence be retained in the loan file to demonstrate this timeline was met. This evidence could include having the borrower electronically sign the document if it is delivered via a compliant E-SIGN process, hand delivering the disclosure and having the borrower sign the document, or mailing the disclosure to the borrower. A common issue occurs when there are several copies of Closing Disclosures in a loan file, and they all have the same date but disclose varying fee amounts. If no evidence is retained in the file to support how these disclosures were delivered to the borrower, it is difficult to determine which disclosures were actually delivered to the borrower and when. This could lead to a delay in closing the loan until the institution is able to obtain adequate evidence that the borrower received the Closing Disclosure timely. Failing to provide Closing Disclosures in a timely manner has the potential to expose the institution to potential litigation from the borrower for not following Regulation Z or could extend the borrower’s right to rescind the loan if the loan is subject to rescission requirements.

8. Including an expiration date of estimated closing costs on revised Loan Estimates

Another common error is including an expiration date of estimated closing costs on revised Loan Estimate disclosures after the borrower has communicated his or her intent to proceed. The CFPB provided guidance in 2017 that this date is to be left blank on revised Loan Estimates after intent to proceed has been communicated since the institution is locked into the fee amounts disclosed to the borrower. As discussed earlier, fees cannot exceed fee tolerance thresholds unless a valid change in circumstance has occurred once an intent to proceed has been received. Loan origination systems vary on how this date can be left blank when required, so it is important that loan personnel understand how this can be accomplished or work with system providers to make this correction.

The CFPB has provided an abundance of guidance for complying with the TRID rules on its website, including a Small Entity Compliance Guide (https://files.consumerfinance.gov/f/documents/2017-10_cfpb_KBYO-Small-Entity-Compliance-Guide_v5.pdf). Detailed FAQs were also updated in May of 2021 to provide clarification on requirements for disclosing Lender Credits, delivering accurate Loan Estimates, complying with TRID rules for housing assistance loans, providing revised Closing Disclosures, and other topics. (See https://www.consumerfinance.gov/compliance/compliance-resources/mortgage-resources/tilarespa-integrated-disclosures/tila-respa-integrateddisclosurefaqs/?_gl=1*1gnownt*_ga*OTkyMTk0NjE5LjE2NDk 3OTUxMDg.*_ga_DBYJL30CHS*MTY1MjM2OTE5Ny44LjEuMTY1MjM2OTI0O.) Management should ensure that employees are aware of the available guidance from the CFPB and are using it as needed to avoid the common errors discussed here.

Conclusion

Loan origination systems can assist in identifying many TRID-related violations, but it is not foolproof. Creditors can decrease the number of exceptions by establishing policies and procedures that provide appropriate guidance to personnel, performing regular training to ensure personnel are knowledgeable about the regulations, and by performing periodic monitoring to confirm that established practices are being followed.

As published in ABA Bank Compliance (now ABA Risk and Compliance), July/August 2022

RELATED