Community Reinvestment Act (CRA) compliance requires a data-driven approach. Though a CRA exam has several important qualitative components, much of a lender’s performance is dependent on what the data shows about the distribution and composition of lending, investments, and services. Accordingly, banks are expected to collect and leverage data to demonstrate how they meet community credit needs and comply with CRA requirements. This article explores three key areas of CRA data analytics and strategy based on CrossCheck Compliance’s CRA analytics and consulting experience:

- Effective collection, testing, and submission of lending data;

- CRA-related metrics and their use in benchmarking; and

- Tools and best practices for monitoring and strategic planning.

Collecting and Testing CRA Lending Data

CRA data collection can be a major undertaking, encompassing Home Mortgage Disclosure Act (HMDA) data, small business and small farm loan data, and tracking of community development (CD) lending, investment, and service activities. Ensuring data integrity at the point of collection is critical – errors in CRA or HMDA Loan Application Registers (LARs) can affect performance assessments and undermine a bank’s credibility with examiners. Robust internal procedures should be in place to capture all required data fields for each reportable loan to assure completeness and accuracy.

Data testing and validation are ongoing processes

Before LAR submission, compliance teams should perform audits, or sample tests, on the data. Root causes of common HMDA and CRA data integrity issues to watch for include misinterpretation of reporting rules, data entry errors, and cursory, as opposed to more comprehensive, monitoring and review. By catching and correcting such issues early, lenders can ensure correct data is submitted and avoid data surprises during exams. Conducting a quarterly “pre-submission” data scrub, where a sample of loans is verified against source documents is a recommended best practice and a similar approach that examiners use. Systemic data integrity reviews of your CRA and HMDA LARs can also be very helpful in identifying data trends and outlier values that require closer scrutiny and potential correction before filing.

Community development activity tracking presents unique challenges

Unlike HMDA, or for large banks, small business, small farm, and community development loans, community development activities are not reported via a standard regulatory form annually; however, they are scrutinized in CRA examinations. Lenders should implement formal tracking systems (even if as simple as a well-structured spreadsheet or database) to log each community development activity and maintain all relevant documentation. Periodic internal reviews of community development activities help ensure these activity candidates for CRA credit are not missed and that each activity submitted to examiners meets the qualifying criteria. In practice, this means that data collection necessitates keeping key information up to date on each activity to document who benefited, where it took place, when it was delivered, and why and how it meets a qualified community need.

Data submission should be seamless if data collection and testing are sound

The Federal Financial Institutions Examination Council (FFIEC) provides free software and a web platform for CRA and HMDA data submissions. Lenders often designate a specific team member (e.g., the CRA Officer, Compliance Officer, etc.) to oversee the annual LAR filings and associated efforts to prepare the data. A smooth submission with minimal errors is often the culmination of months of effort.

Measuring Performance with CRA Data Analytics

Measuring CRA performance should be based on lending and community development data that is organized into statistical tables that mirror what are typically prepared by CRA examiners. Using internal data blended with public data necessary for benchmarking is a sound and best-practice approach to this data organization. Lenders can download aggregate HMDA and CRA lending data, branch office deposits, peer Call Report data, and demographic data for assessment areas. Due to the challenges of bringing these disparate data sources together to evaluate performance, many lenders rely on consultants to conduct analyses and address gaps that industry software may not always accurately identify and fully resolve.

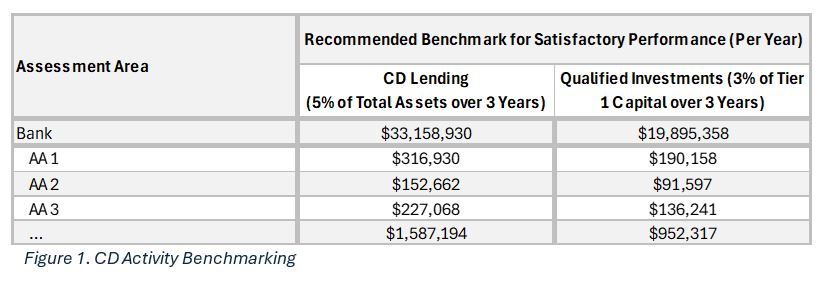

Peer benchmarking and scenario analysis are crucial for effective CRA analytics

Many CRA performance criteria rely on comparative analyses. For example, a HMDA reporter should analyze how its percentage of loans in low- to moderate-income (LMI) areas compares to the aggregate lending in its assessment areas. However, there are no performance standards under the current CRA rule that lenders can rely on to understand how its measured performance actually translates to CRA ratings. What does a percentage of lending to LMI tracts that is 90 percent of the aggregate percentage mean in terms of the bank’s expected rating for that criterion? What would 60 percent mean?

Financial institutions can address this gap in CRA data analytics by collecting data in published performance evaluations for similarly situated peers to understand the range of performance levels and their corresponding ratings from examiners. While there is no automated, industry-standard solution for extracting this data, institutions can manually track key performance indicators – such as the number and dollar amount of qualified investments, Tier One Capital, exam cycle length, and the assigned performance rating for the criterion – in a spreadsheet or database. This allows for normalized benchmarking using performance ratios (e.g., dollar amount of investments divided by Tier One Capital, adjusted for exam cycle length) to learn how the lender’s performance ratio compares to the range of peer ratios and their corresponding ratings.

When there is some meaningful uncertainty, the lender can run scenario analyses to make final assessments of performance by considering the implications of educated assumptions based on research and analyses. For example, a lender evaluated under Large Bank procedures with lending to LMI census tracts that hovers between a “Low Satisfactory” and “Needs to Improve” threshold might model the impact of each possible rating on the Lending Test and Overall rating using the regulator’s point-based exam procedures. Such a comprehensive analysis prepares management with data-backed insights for strategic decisions based on the likeliest performance ratings.

Tools, Mapping, and Strategic Planning for CRA

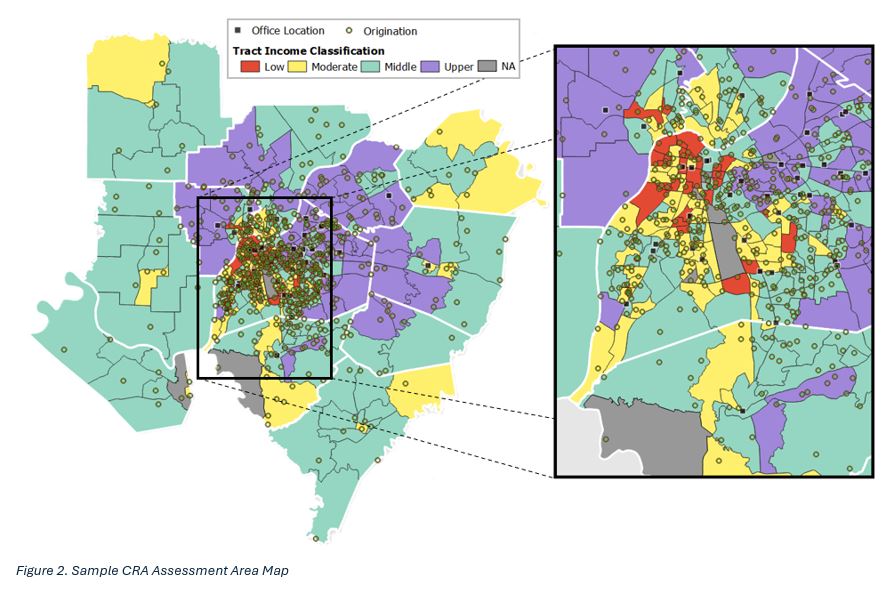

CRA compliance today is greatly aided by technology and analytics tools. Many lenders invest in software solutions (or in-house systems) to manage CRA and HMDA data. These tools typically offer features such as automated geocoding, built-in edit checks for reporting errors, and the ability to generate required submission files. The tools often include mapping modules that provide visualizations of applications, originated loans, branches, and assessment area boundaries on a map.

For example, a CRA officer can plot a bank’s mortgage and small business loans over a map of census tracts color-coded by income level – quickly seeing how well the bank is serving LMI areas. Mapping is also a crucial tool that can help banks spot gaps in coverage or potential “hot spots” for community development. In some cases, maps reveal a red flag doughnut hole pattern, an area in the middle of a city where the lender has little activity surrounded by areas where it lends more actively. These insights can directly inform a lender’s strategic planning.

Beyond mapping, lenders use analytical dashboards and databases to track their CRA performance across multiple years. Such software can be extremely helpful; however, it is not a substitute for good procedures and data discipline. Lenders can utilize the most modern CRA compliance software but still stumble in exams because the data input was incomplete, the staff did not interpret the reports correctly, or the staff did not have the training or time to effectively use their systems. Alternatively, lenders with modest tools (including relying on spreadsheets) but strong internal governance often excel in CRA compliance. Ideally, management seeks to benefit from both, balancing quality data and robust processes, enhanced by technology that makes analysis easier and more visual.

Best practices to consider when leveraging CRA technology data analytics include:

- Integrating data sources: Combine lending, community development, branch, demographic, economic and other relevant data for the most complete picture of performance.

- Identifying community development opportunities: Use internal and external data to find where community development financing or services are needed. The investigation could include analyzing which parts of the assessment area have few affordable housing projects or which local nonprofits might benefit from partnerships.

- Scenario planning: Scenario analysis can be a powerful feature of CRA planning. In addition to helping to assess past performance, scenario analysis such as simulation modeling can forecast how changes (opening or closing branches, launching a special loan program, adjusting assessment area boundaries, etc.) might affect CRA performance measures.

- Mining Performance Evaluations (PEs) for insights: Public CRA PEs contain valuable unstructured data, including granular performance ratings at the test and criterion level, examiner comments, and context for ratings that are not readily available in structured datasets. Systematically reviewing and extracting this information can enhance peer benchmarking, clarify performance expectations, and support more accurate assessments and scenario planning.

- Regular monitoring via dashboards: Rather than waiting for year-end, lenders should track CRA metrics quarterly or even monthly. Simple spreadsheets or industry tools allow setting up dashboards that show year-to-date lending by assessment area, progress toward goals (e.g., number of community development investments made), and how the distribution of loans compares to demographic and aggregate benchmarks.

- Aligning CRA analytics with incentives: CRA performance data can be used to support incentive-based programs that reward lenders for contributing to community development goals. By integrating CRA metrics as a complement to traditional production-based compensation or recognition programs, institutions can better align lending and service activities with their community impact objectives.

Turning CRA Analytics into Competitive Advantage

Lenders that leverage their data effectively – from accurate collection and geocoding, to thoughtful analysis and mapping – put themselves in the best position to meet these expectations around demonstrating a clear understanding of their performance context, proactively identifying community needs, and supporting data-driven CRA strategies. By diligently collecting and testing HMDA and CRA lending data, understanding, and using publicly available metrics for context, and deploying tools (along with strong procedures) for ongoing tracking and planning, an institution can transform CRA compliance into a strategic advantage. Lenders that treat CRA data analytics as an integral part of their business strategy can achieve better exam results while uncovering new opportunities to serve their communities. In the end, CRA performance is strong when informed analytics guide confident action, ensuring that resources make a meaningful impact where they matter most.

At CrossCheck Compliance, we are committed to helping lenders manage CRA compliance with confidence. Learn how our performance assessment, data integrity, and advisory services can guide your organization through examinations, performance context development, and strategic planning.

Contact Us Today for More Information

Authored by Jonathon Neil