Advances in machine learning and artificial intelligence (AI) in credit underwriting and pricing have created substantial opportunities for lenders. While machine learning has been used for years in credit score modeling and automated underwriting systems within mortgage lending, recent advances in AI – including more complex credit scoring systems, third-party AI platforms, and adaptive large language models – have introduced new compliance risks that are harder to detect and explain.

Sample client questions:

- “How can we test for fair lending risk if we use an external vendor model?”

- “Does the AI score threshold that we set create disparities?”

- “What is our fair lending risk exposure when our underwriters override the AI decision?”

These developments allow lenders to enhance profitability and expand access to credit among historically underserved segments by analyzing more data points and generating more granular decisions. The increasing integration of this technology, however, also creates additional compliance challenges, presenting new avenues for fair lending risk to emerge. The dynamic regulatory environment at the federal and state levels presents another obstacle. Lenders using or exploring AI underwriting must be prepared to evaluate their models and decision-making processes in anticipation of regulatory scrutiny.

Many of these fair lending compliance risks were explored in a recent CrossCheck article and are already subject to regulatory scrutiny, including a notable settlement between the Massachusetts Attorney General and a FinTech lender specializing in student loans. Published papers on the selection of less discriminatory algorithms and the AI’s influence on “digital redlining” are recent examples of researchers contributing to the growing dialogue on AI fairness in financial services, highlighting the salience of the topic.

The increased complexity introduced by AI systems into the decision-making process requires a flexible solution that can isolate risk across different components of that process. CrossCheck has developed an analytic framework and other services to meet this emerging need among clients.

AI Fair Lending Performance Analysis: Identifying Disparities Across the Credit Decision Funnel

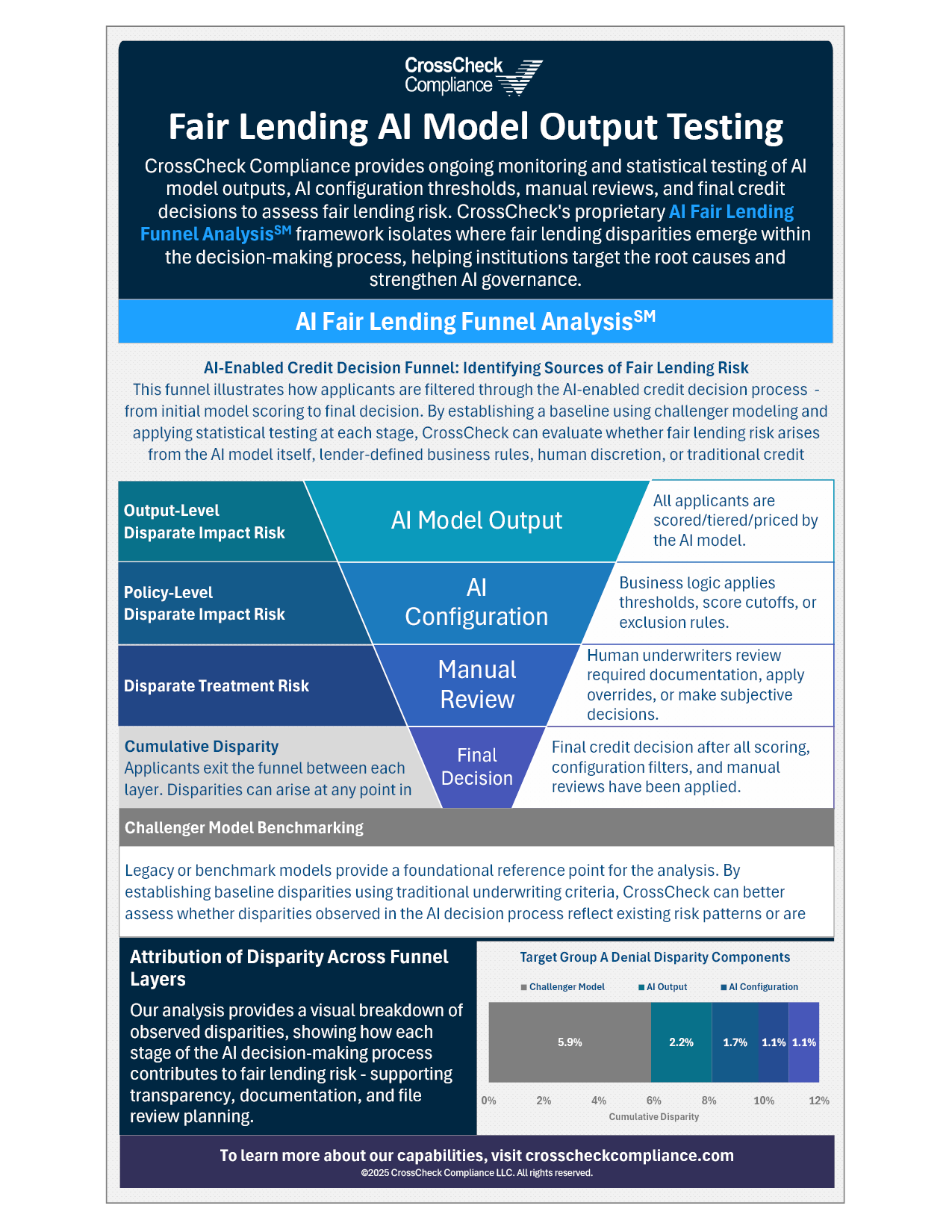

CrossCheck uses a proprietary framework – the AI Fair Lending Funnel AnalysisSM – to help lenders identify sources of potential disparities across the full credit decision process. This framework accommodates how clients incorporate proprietary or third-party AI systems into their processes, which generally comprises up to four stages of a decision funnel:

- AI Model Output: Every applicant is scored, tiered, decisioned, or priced by the model.

- AI Configuration: The lender applies business logic to the AI output, such as thresholds, auto-decisioning, and applicant segmentation.

- Manual Review: Human underwriters assess documents, make overrides, or issue judgements on a subset or all applications.

- Final Decision: The lender makes a final underwriting or pricing decision after all filters, reviews, and processes.

Conducting statistical testing at each stage of the credit decision funnel helps lenders identify whether disparities are associated with the AI model itself, with how the model is used by the lender, or from manual decisions made later in the process.

Adverse Action Reason Testing

Validating whether stated reasons for credit denial align with actual decision drivers, both in the system and the AI model, is important, as discrepancies can result in legal exposure under the Equal Credit Opportunities Act (ECOA) and the Fair Credit Reporting Act (FCRA).

AI Vendor Oversight Review

When lenders rely on third-party AI providers, vendor oversight becomes a necessary compliance function. Solution and systems documentation, data usage disclosures, and model governance controls should be reviewed to assess regulatory alignment.

AI Model Explainability Review

A key consideration in AI model governance is the ability to meaningfully explain AI model outputs and assess the consistency of those explanations with observed patterns. Lenders should review available documentation and explainability tools to evaluate whether the lender is able to meet regulatory expectations and internal standards.

A Practical Approach to AI Fair Lending Risk

Though machine learning has an established history in credit decision-making, AI is fundamentally transforming those processes. The technology holds promise of expanding access to credit while enhancing business value (e.g., lower credit risk, operational efficiency, higher profit, etc.); however, it does not eliminate fair lending risk. Instead, AI models can shift risk into upstream components of the credit decision process. Compliance teams managing AI-enabled systems must stay ahead by using structured, layered analyses such as the AI Fair Lending Funnel AnalysisSM augmented by sufficient governance programs. Whether your institution is piloting AI, scaling its use, or preparing for an exam, a robust AI fair lending compliance framework is essential to demonstrate effective controls in this dynamic regulatory landscape.

Contact us to explore how CrossCheck can support your organization in proactively managing AI-related fair lending risks and strengthening regulatory readiness.

Authored by Jonathon Neil