In recent years, financial institutions have faced increasing scrutiny of their compliance with fair lending laws. One emerging and critical component of meeting regulatory expectations is conducting a Community Credit Needs Assessment (CCNA). A CCNA plays a pivotal role in identifying and addressing the financial needs of historically marginalized and under-resourced communities, including majority-minority and low-to-moderate-income census tracts in a lender’s market area. Drawing from key requirements outlined in redlining consent orders that have been brought forth by the U.S. Department of Justice (DOJ) over the past three years, outlined below are the expectations for a CCNA.

What Is a Community Credit Needs Assessment?

A CCNA is a research-based market study designed to help lenders understand and meet the financial service needs of specific, focal point communities in a specific market area. The primary goal of the assessment is to ensure that lenders are identifying gaps in credit availability and implementing strategies to address these gaps. By proactively assessing and addressing community needs, lenders can enhance access to credit and financial inclusion in their lending and banking practices while meeting regulatory obligations.

Key Components of a Community Credit Needs Assessment for Mortgage Lending

To align with regulatory expectations, a CCNA must include several essential elements, and based on DOJ requirements, these elements should include specific components.

1. Evaluation of Residential Mortgage Credit Needs and Lending Opportunities

This element involves conducting quantitative analysis, interviews of community contacts, and qualitative research to evaluate the credit needs within the focal point communities in the lender’s market area. Key questions to explore include:

- What are the barriers that lower income individuals and households face in accessing credit and participating in the traditional financial system?

- What types of residential mortgage products are most needed in these communities?

- Are there existing gaps in the availability of lending services?

An analysis of current lending opportunities helps identify underserved areas and prioritize strategic interventions.

Figure 1. Developing a profile of the community

2. Demographic, Socioeconomic, and Language Data

A robust assessment requires the inclusion of recent demographic and socioeconomic data for the targeted census tracts within the lender’s market area. Key topics include:

- Demographic and language composition of the population.

- Housing characteristics and affordability indicators.

- Income levels, employment statistics, and socioeconomic status.

This data provides the foundation for tailoring lending products and outreach efforts to the unique needs of the community.

3. Strategies for Providing Residential Mortgage Products and Lending Services

The assessment must outline potential strategies for expanding access to residential mortgage products and services in the identified census tracts. Examples might include:

- Offering specialized loan products for first-time homebuyers.

- Partnering with community organizations to build trust and awareness.

- Enhancing digital access to mortgage services for underserved populations.

4. Language Accessibility

A critical aspect of the assessment involves evaluating the need to provide marketing materials and loan origination documents for populations with limited English proficiency (LEP). For communities with significant non-English-speaking populations, language accessibility is essential for ensuring equitable access to financial services. Recommendations should address:

- Translation of marketing and loan documents.

- Hiring bilingual staff or providing language training for existing staff.

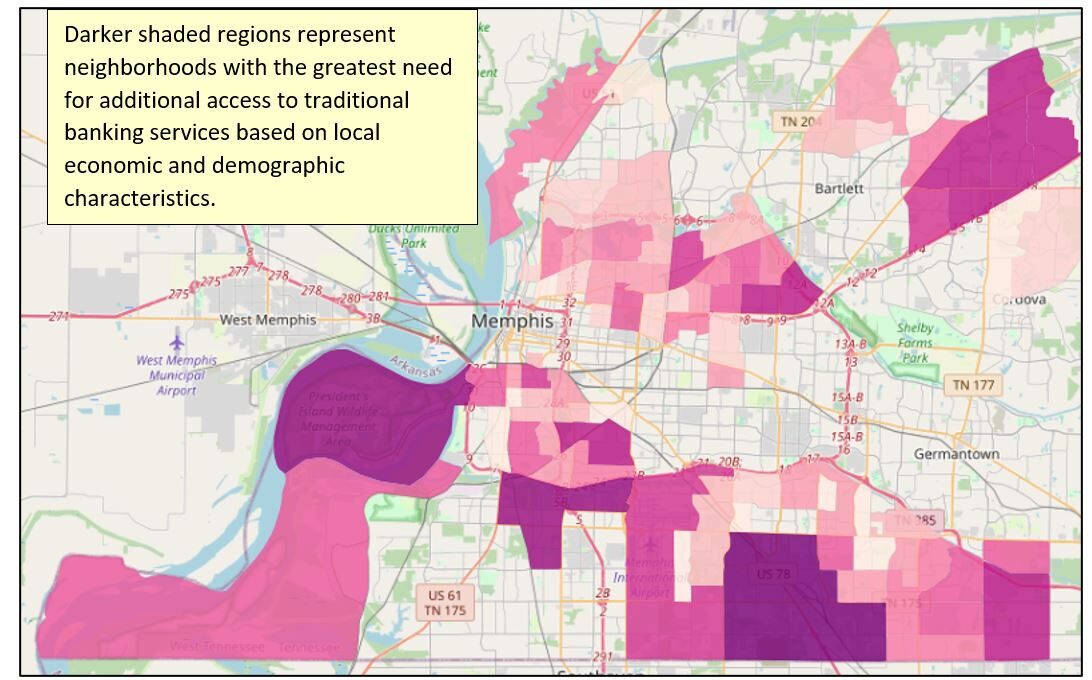

5. Branch Locations in Underserved Areas

The CCNA must assess the potential for establishing new branches in underserved areas, particularly in minority communities in densely populated urban areas. This assessment includes:

- Identifying geographic gaps in branch locations.

- Discovering suitable locations based on community needs, accessibility, and commercial viability.

Figure 2. Access to Traditional Depositories in Majority-Minority Census Tracts

6. Competitor Analysis

A review of residential mortgage products and services offered by other lenders in the market is another critical component. This analysis should address:

- What strategies have been successful for competitors?

- Have competitors launched portfolio affordable mortgage products, including Special Purpose Credit Programs, in the market area?

- How do competitors’ products and lending practices compare to those offered by the institution?

Understanding the competitive landscape can help inform the lender’s strategy and highlight areas for differentiation.

7. Federal, State, and Local Programs

An overview of government programs available to residents seeking residential mortgage loans is essential. Examples include:

- Government insured loan programs (i.e., FHA, VA, and USDA).

- Affordable programs offered by Fannie Mae, Freddie Mac, and regional federal home loan banks.

- State-sponsored down payment assistance initiatives.

- Local grants or incentives for first-time homebuyers.

By leveraging these programs, lenders can better meet community needs and increase access to credit.

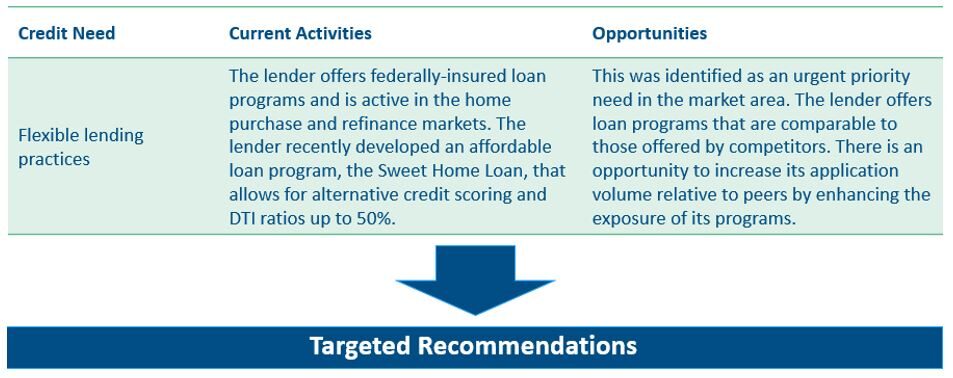

8. Opportunities and Recommendations

Finally, the assessment must include actionable recommendations for how the lender can address identified community credit needs and, if applicable, meet its obligations under a supervisory action or consent order. These recommendations should focus on opportunities to address the identified community credit needs and achieve the desired goals, accounting for the institution’s existing or planned initiatives.

Figure 3. Discovering Opportunities to Address Needs

Why Community Credit Needs Assessments Matter

CCNAs are more than just compliance tools—they serve as valuable resources for driving positive changes in underserved communities. By identifying and addressing barriers to credit, financial institutions can:

- Build trust and strengthen relationships with marginalized and under-resourced communities.

- Foster economic growth and homeownership in historically underserved areas.

- Demonstrate their commitment to fair lending practices.

A well-executed CCNA provides a roadmap for financial institutions to meet both regulatory and community expectations. By incorporating comprehensive data analysis, qualitative research, and actionable recommendations, these assessments help bridge gaps in access to credit and promote greater access to credit and the corresponding economic and social benefits.

Understanding the key elements of a CCNA is an essential tool for guiding financial institutions toward success in meeting their obligations and supporting community development goals. By understanding regulatory expectations, institutions can achieve compliance under fair lending laws and the Community Reinvestment Act, as well as contribute to lasting positive changes in the communities they serve.

Authored by Jonathon Neil | February 2025