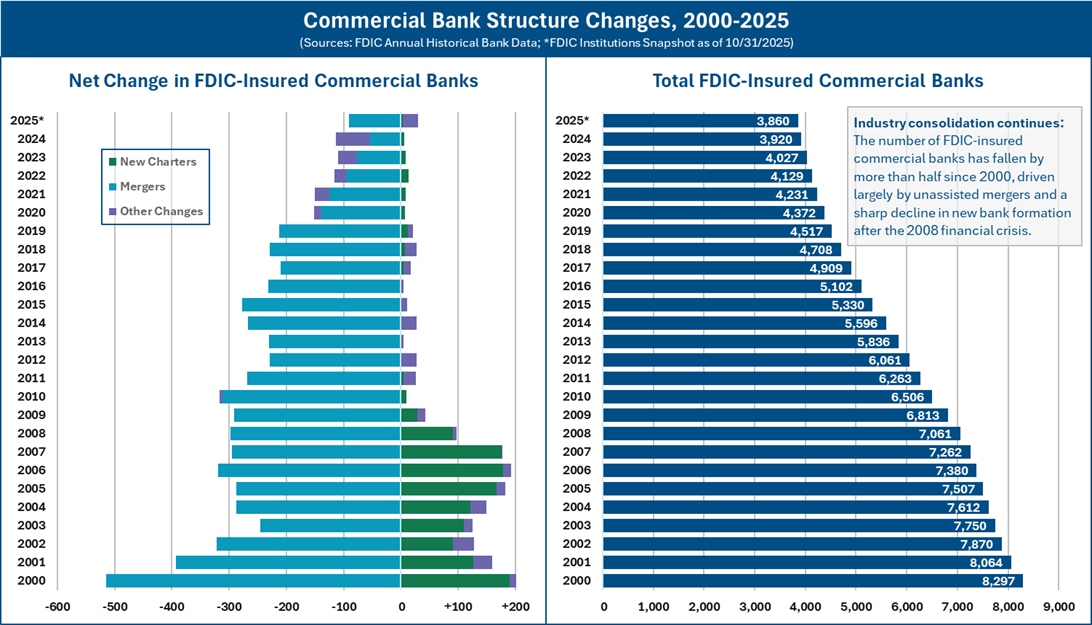

As merger and acquisition activity accelerates in the banking sector, institutions are rediscovering that community reinvestment and credit access obligations are not separate considerations from the deal itself. As shown in Figure 1, the number of FDIC-insured commercial banks has declined by more than half since 2000, driven largely by sustained consolidation and a sharp slowdown in new bank formation following the financial crisis. While this structural shift has unfolded gradually over decades, its regulatory implications are increasingly immediate. Federal agencies, state regulators, and community organizations continue to scrutinize these transactions, ensuring that local lending and service obligations remain central to merger reviews. Even in a changing enforcement climate, the Community Reinvestment Act (CRA) and fair lending expectations still determine how smoothly a transaction proceeds and how it is received in the communities it affects.

Figure 1. Commercial Bank Structural Changes, 2000-2025

The Regulatory and Stakeholder Context

Under the existing CRA framework, regulators continue to evaluate mergers for their impact on the convenience and needs of the community. While priorities can change with each federal administration, the core legal framework remains firmly in place. CRA performance records, fair lending histories, and public input remain integral parts of each merger application.

Meanwhile, state regulators and community organizations have taken an active role in M&A processes. Advocacy groups and local officials can – and often do – submit comments, hold hearings, or question merger applications that they believe could reduce access to credit or banking services. For many banks, that external pressure can shape merger timelines or the conditions of approval more than the formal regulatory review itself.

Key CRA and Fair Lending Risk Areas in M&A

Mergers introduce both opportunity and risk under the CRA and fair lending requirements. The most common pressure points include:

Geographic market expansion

When a merger introduces new assessment areas or lending markets – especially where one institution has limited prior presence – the combined bank must ensure that low- and moderate-income (LMI), majority-minority communities, and small businesses and farms are appropriately served. Overlooking emerging community needs can lead to service gaps and even raise concerns about practices like redlining.

Product and segment expansion

Entering new credit products and categories can shift the profile of lending distribution and fair lending exposure. Differences in product composition and pricing, underwriting, or marketing practices may surface as risks once portfolios are combined.

CRA and fair lending record disparities

When two merging institutions have uneven CRA ratings or historical exam findings, those differences can lead to regulatory scrutiny. Even without geographic expansion, either party’s fair lending history can complicate approval or invite community objections.

Branch optimization and access

Overlapping branch networks often lead to consolidation. Without a plan to maintain access in LMI or majority-minority neighborhoods, such changes can draw criticism and heighten risk of community opposition that creates transaction friction.

Preparing for Review: A Forward-Looking Approach

Institutions that treat CRA and fair lending as part of the strategic due-diligence process, rather than as post-merger compliance steps, can navigate the review process more effectively. Some practical steps can make a measurable difference:

- Conduct a comprehensive CRA self-assessment and fair lending review early. Evaluate each party’s CRA ratings, public evaluations, exam findings, and performance context. Identify any gaps in branch coverage or lending distribution, particularly in overlapping or newly created assessment areas.

- Perform a community credit-needs assessment (CCNA) that spans both institutions’ footprints. Using CRA and Home Mortgage Disclosure Act data, assess how credit demand, demographics, and community needs align with your business model and capacity. This analysis also reveals underserved markets that could become strategically important post-merger.

- Use forecasting and scenario planning to anticipate how compliance risk may evolve. Modeling possible outcomes – such as how branch changes, product shifts, or demographic trends might alter CRA or fair lending metrics – helps leadership see whether risk is introduced or is likely to fade or grow, and where proactive steps could mitigate it.

- Integrate findings into the merger narrative and community plan. Document your analysis, commitments, and engagement efforts to demonstrate that the transaction strengthens, rather than weaknesses, service to local markets. If potential issues are identified, outline the plan to address those concerns. Open, honest conversations with community groups and regulators go a long way in building trust and avoiding pushback.

CRA and Fair Lending as a Strategic Foundation for M&A Success

CRA and fair lending compliance should not be treated as just another box to tick after a deal is done. They are foundational components of risk management and long-term market strength. Banks that embed community credit and access considerations into their M&A strategy – through assessment, forecasting, and transparent engagement – position themselves for smoother approvals and stronger community trust.

By looking beyond the transaction itself and toward the communities affected by it, institutions demonstrate not only compliance readiness but also leadership in equitable growth.

Contact CrossCheck to integrate CRA and fair lending considerations into your M&A strategy, strengthening regulatory readiness and long-term community trust.

Authored by Jonathon Neil

Related Articles

- Measuring and Maximizing CRA Performance Through Data Analytics

- Fair Lending Risk in AI Credit Models: A Compliance Framework for Lenders

- From Automated Underwriting to Artificial Intelligence: How Fair Lending Risk Oversight Must Evolve